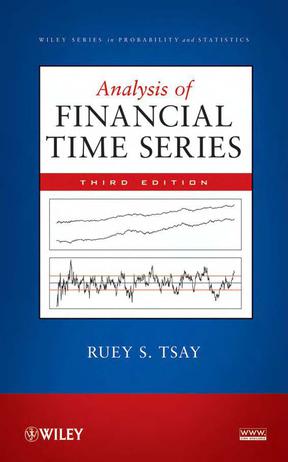

Analysis of Financial Time Seriestxt,chm,pdf,epub,mobi下载 Analysis of Financial Time Seriestxt,chm,pdf,epub,mobi下载

作者:Ruey S. Tsay

出版社: Wiley

副标题: Third Edition

出版年: 2010-09-21

页数: 677

定价: USD 120.00

装帧: Hardcover

丛书: Wiley Series in Probability and Statistics

ISBN: 9780470414354

内容简介 · · · · · ·This book provides a broad, mature, and systematic introduction to current financial econometric models and their applications to modeling and prediction of financial time series data. It utilizes real-world examples and real financial data throughout the book to apply the models and methods described. The author begins with basic characteristics of financial time series data b...

This book provides a broad, mature, and systematic introduction to current financial econometric models and their applications to modeling and prediction of financial time series data. It utilizes real-world examples and real financial data throughout the book to apply the models and methods described. The author begins with basic characteristics of financial time series data before covering three main topics: Analysis and application of univariate financial time series The return series of multiple assets Bayesian inference in finance methods Key features of the new edition include additional coverage of modern day topics such as arbitrage, pair trading, realized volatility, and credit risk modeling; a smooth transition from S-Plus to R; and expanded empirical financial data sets. The overall objective of the book is to provide some knowledge of financial time series, introduce some statistical tools useful for analyzing these series and gain experience in financial applications of various econometric methods.

作者简介 · · · · · ·Ruey S,Tsay(蔡瑞胸),美国芝加哥大学布斯商学院经济计量及统计学的H G.B.Alexande r讲席教授。1 982年于美国威斯康星大学麦迪逊分校获得统计学博士学位。中国台湾“中央研究院”院士,美国统计协会和数理统计学会的会士,Journal of Forecastin9的联合主编,Journal of FinancialEconometrics的副主编。曾任美国统计学会商务与经济统计分会主席、《商务与经济统计》期刊主编。

|

首页

首页

原以为会很枯燥

看完,超赞

什么也不说了